The big economic news from this past week was that inflation readings came in nice and cool for the month of May. The Fed decided to keep the benchmark interest rate (the Federal Funds Rate) unchanged in the range of 5.25-5.50%.

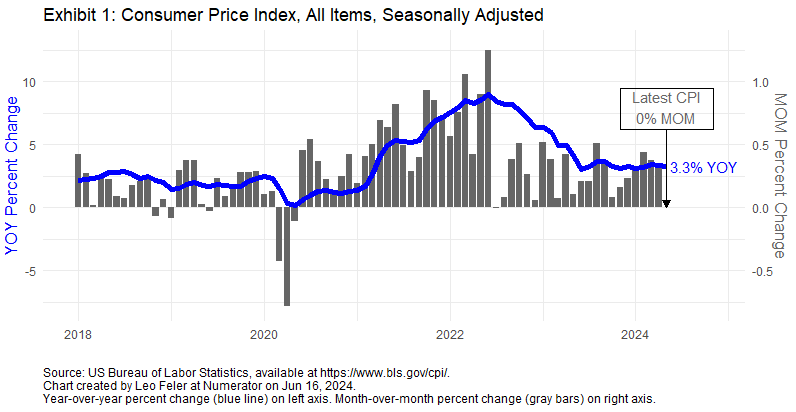

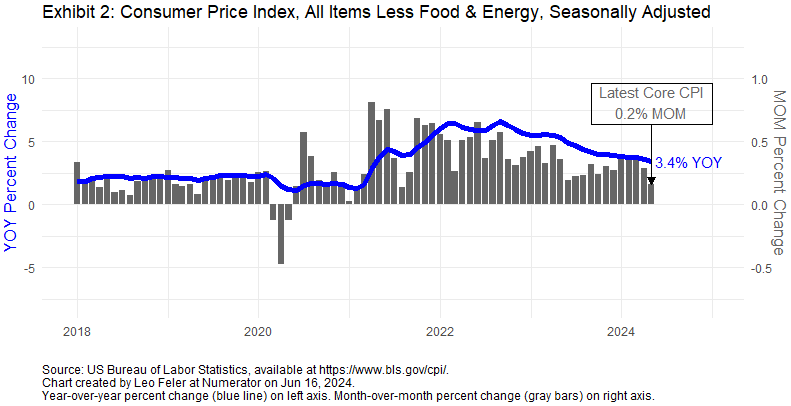

Total consumer price inflation came in at 0.0% month-over-month, the lowest reading in nearly two years. Excluding food & energy, the core CPI came in at 0.2% month-over-month, the lowest reading in nearly three years. This means consumer price inflation now stands at 3.3% versus a year ago, and core CPI now stands at 3.4% versus a year ago.

A question I hear often is why exclude food & energy from inflation measures when they represent approximately 20% of the consumer basket? The answer is that, while food & energy inflation is certainly important for consumers, it’s so volatile that it doesn’t provide a good signal of underlying inflation, how sticky inflation is, or where inflation might be headed in the coming months. So economists and the Fed prefer to exclude food & energy inflation and look at the “core” CPI for a better, less noisy understanding of underlying inflation trends.

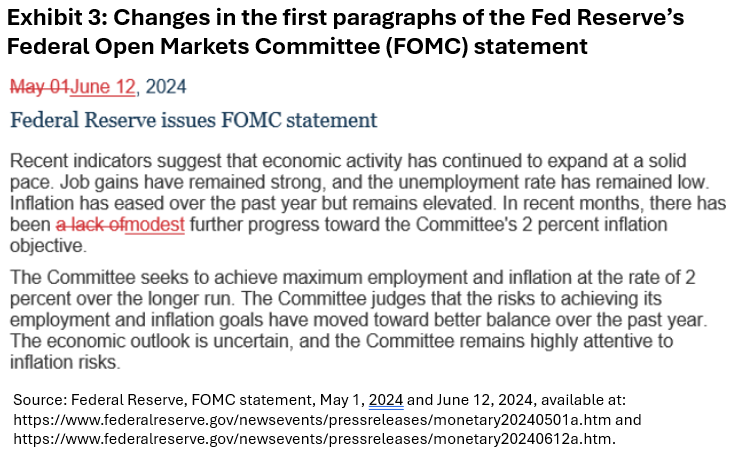

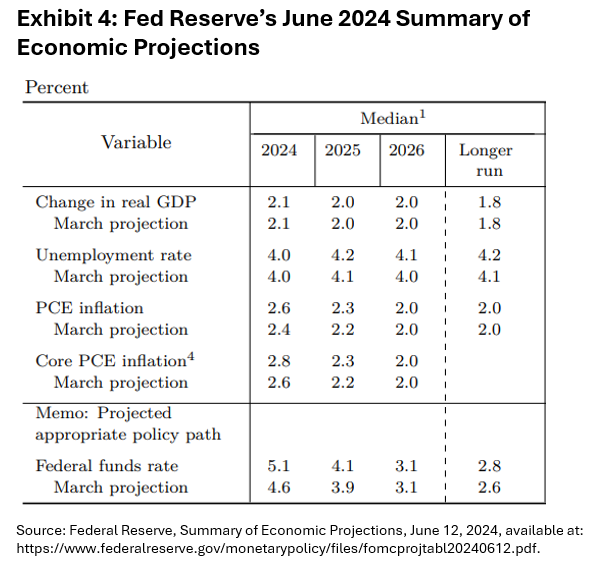

The underlying inflation trends so far this year suggest there has been “modest further progress” toward the Federal Reserve’s 2% inflation target. The latest Fed statement replaces “lack of further progress” with “modest further progress”. So we have some progress, just not enough progress to provide sufficient confidence that inflation is heading sustainably down to the Fed’s 2% target. As a result, the Fed decided to keep interest rates unchanged during its monetary policy meeting this week, and more importantly, it signaled in its quarterly Summary of Economic Projections (SEP), that it would keep rates high for a longer period of time. The Fed is now signaling that the median participant on its Federal Open Markets Committee, which sets the benchmark interest rate, expects only one 25 basis point cut by the end of the year, which would leave the benchmark rate at 5.0-5.25% by year-end, versus 4.5-4.75% projected previously in the March SEP.

The Fed also expects the economy to grow 2.1% during 2024, the unemployment rate to be 4.0% by the end of 2024, and core PCE inflation to be 2.8% year-over-year in Q4 2024 (up from 2.6% from its March projection).

A quick aside: the Fed’s target is 2.0% annual core PCE inflation. What’s the difference between core PCE inflation and core CPI inflation? Both exclude food & energy. The shorthand I use to understand the difference is CPI is based on what consumers buy themselves; Personal Consumption Expenditure (PCE) is based on what consumers consume, regardless of whether they’re the ones buying it. The key difference comes from healthcare. Consumers consume healthcare, but for many of us, it’s bought for us by our employers (through employer-provided health insurance) rather than something we buy ourselves. Healthcare is a big component of personal consumption expenditures, even though it’s not something we tend to “buy” per se. There are other differences between the CPI and PCE measures of inflation, but this is the main one. When the CPI runs at about 2.2-2.4% per year, the PCE measure runs at about 2.0%.

Now back to the Fed. The fact that the Fed expects the same amount of economic growth this year with fewer rate cuts, the same unemployment rate, but slightly higher inflation suggests the economy is proving to be more resilient and inflation is proving to be a bit more sticky than previously expected. And that means the Fed can keep rates higher for longer in order to get inflation back down to its target without as much of a downside risk to the economy.

I think the higher-than-expected inflation readings we saw in the first three months of this year were a bit of a fluke – a few lagging sectors, like housing and auto insurance, continuing to reset prices to market rates – rather than a true re-acceleration of inflation. We should now continue to see disinflation, just like we saw these past two months, which means the Fed should have enough confidence in its victory over the inflation battle to start cutting rates in September, and potentially a second cut at the end of the year. But we’ll see how the economic data develops. The Fed continues to say it is “data dependent” which means we’re at the mercy of incoming data, and as we know, data can be noisy and imperfect.